Araya Doheny

MicroStrategy (NASDAQ:MSTR) is up from near-term lows as Bitcoin shakes wider fears around the retrenchment of the crypto space to warm up from a long winter. Not even the chapter 11 bankruptcy filing of Genesis, Digital Currency Group’s crypto lender, could stop the price of Bitcoin from pushing above $20,000.

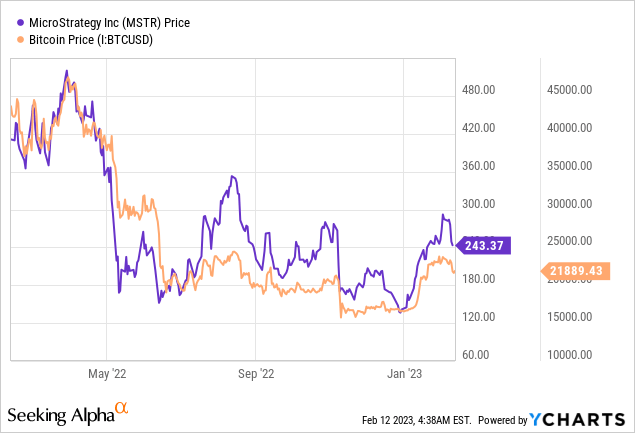

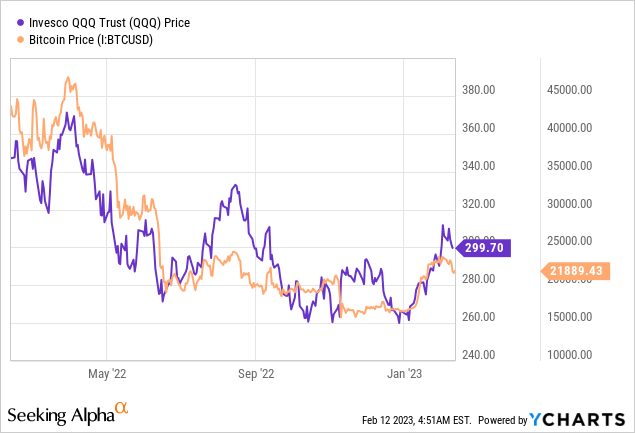

Its investors, speculators, and maximalist now looking at broader macroeconomic figures for direction. Indeed, the economic story of the last 12 months has been defined by elevated inflation, rising Fed fund rates, and the specter of a recession. Why is this relevant for bitcoin? The digital asset has been tracking the performance of the tech-heavy Nasdaq 100 index for a while.

MicroStrategy is essentially a proxy for a direct Bitcoin investment in lieu of a spot bitcoin ETF. Hence, I think the direction of inflation, interest rates, and the US economy will likely be the biggest driver of Bitcoin returns this year. Essentially, a return of animal spirits on the back of a seemingly dovish pivot by the Fed as inflation cools back to their 2% target rate will be the most material determinant of where MicroStrategy is trading at the end of the year.

To be clear here, Bitcoin essentially fell from its highs during the pandemic just as tech, SPACs, and growth stocks collapsed. The golden era then was defined by highly jubilant animal spirits as heavy pandemic-era stimulus programs pumped liquidity into the markets. This of course changed with the energy crisis and Russia’s war in Ukraine, which stoked inflation and forced the Fed to embark on the most aggressive tightening program in decades.

The Fiscal 2022 Fourth Quarter Earnings

MicroStrategy operates around two corporate strategies. The first is an operating strategy constructed on the back of its Business Intelligence software business. The second is a balance sheet strategy built around their adoption of Bitcoin as a primary treasury reserve asset. MicroStrategy aims to buy Bitcoin and hold for the long term using excess cash generated from its operating strategy as well as proceeds of capital-raising transactions.

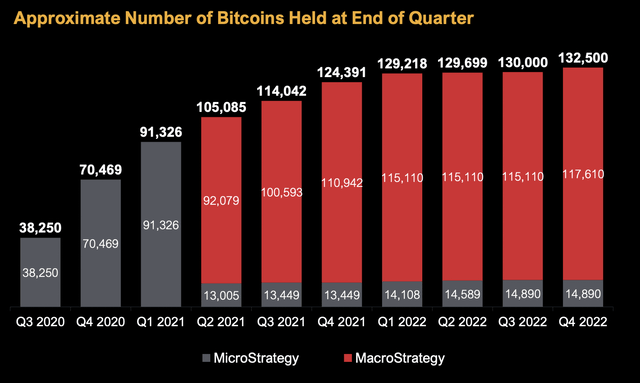

The company’s recently reported earnings for its fiscal 2022 fourth quarter saw revenue come in at $132.6 million, a decline of 1.4% from the year-ago period but still a beat by $1.6 million on consensus estimates. MicroStrategy held 132,500 Bitcoins as of the end of the quarter, growing by 2,500 sequentially from the prior third quarter.

MicroStrategy

This had a carrying value of $1.840 billion and a cumulative impairment loss of $2.15 billion. The current market value of MicroStrategy’s Bitcoin holdings now stands at $2.9 billion, up 32.4% from $2.19 billion as of the end of the fourth quarter. The company’s purchase of 2,500 Bitcoin during the quarter was completed for a net aggregate purchase amount of $45 million, around $17,850 per Bitcoin. With MicroStrategy now up on this specific tranche of Bitcoin purchases, bulls will be hoping the value of the digital asset pushes above MicroStrategy’s average cost per Bitcoin of $30,137.

The Dual Strategy And The Future Of Bitcoin

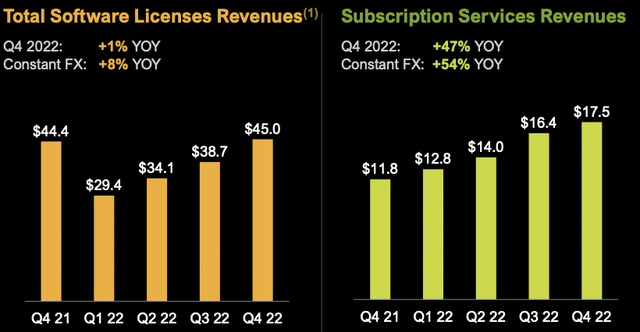

The core software business generated gross profits of $105.8 million, down from $110.5 million in the year-ago quarter, as gross profit margin fell by 240 basis points to 79.8%. This decline still came on the back of subscription service revenue that grew by 47% year-over-year to reach $17.5 million.

MicroStrategy

This also came with a high 95% renewal rate during the quarter, up from five consecutive quarters where the company notched a 90% renewal rate. MicroStrategy would realize a net loss of $193.7 million during the fourth quarter, up from $137.5 million in the year-ago comp and driven by a Bitcoin impairment loss of $197.6 million. Cash from operations was negative at $18.2 million, a decline from positive cash flow of $3.2 million in the year-ago quarter. This helped drive cash and equivalents lower to $43.8 million versus $60.4 million in the year-ago period.

Of course, MicroStrategy could dispose of Bitcoin at any time to shore up its balance sheet, so the runway is not uncertain under any terms. The risk here will come from its inability to buy Bitcoin with positive cash flows in future quarters as per its strategy. The company initiated a $500 million at-the-market (ATM) equity offering during the quarter and raised approximately $46.6 million in gross proceeds, with $453 million left outstanding under the ATM. Dilution to buy assets that you lose money on if Bitcoin returns to its near-term lows would not be a shareholder-friendly strategy.

MicroStrategy’s bulls are also looking towards the next Bitcoin halving for a further recovery of positive sentiment. This is a pivotal event that cuts the reward for mining Bitcoin in half to reduce the supply and, hence, the inflation of Bitcoin. This is more than a year away, around March 18, 2024. In the near term, bulls will be hoping the current dynamic with falling inflation and peaking Fed fund rates continues to spark a return of jubilant animal spirits. I remain neutral on the company.